We have been witnessing for a whole year how Wall Street listens in suspense to every word that Jerome Powell releases in his press conferences. And the worst of all is that, since the beginning of 2021, it was known that the Fed would raise interest rates sooner rather than later. Now, after all the craziness at the beginning of 2022, we are going to take a look at history to see what usually happens in the market when interest rates rise.

Just to make it clear from the start. Obviously, anything can happen in the market and what has happened in the past does not have to be repeated in the future. Even so, history can give us clues and that is why we are going to get into it to see what we find.

Table of Contents

Let’s start at the beginning (forgive the redundancy)

What interests will the Fed raise? The mortgages? Personal loans? The credit cards? Directly, none of the above.

When we talk about the Fed raising interest rates, we are actually talking about something called the Federal Funds Rate, which is the interest charged by one bank to another for lending money to each other, the so-called overnight loans.

Obviously, if it costs a bank more money to access capital, it will raise the interest on the products they offer to the public (mortgages, personal loans, credit cards, etc.) to compensate.

It is for this reason that it is expected that when the Fed raises the rates of the blissful Federal Fund Rate, everything else will be affected, including the financing of companies; Which is why growth stocks, which need to be heavily funded, suffer in this environment.

Now, the interest benchmark, today, in the United States is between 0 and 0.25%, the lowest point, in the period after the 2008 crisis, since 1971.

It is estimated that the Fed will raise interest rates about 5 times in 2022 and that each increase will be an average of 0.25%. That could place us in a scenario of an interesting benchmark of 1.50% in the worst case, although some point out that we could reach between 1.75% and 2%.

It is clear that a rise of almost 10 times the current range seems a bit radical but watch this.

So, in perspective, even if the Fed has to tighten the screws to curb inflation and raises interest rates to 2%, we are well below the historical average. So the world is not ending.

How does the market usually react?

The market as such, in an environment of high-interest rates, is not conducive to looking at it as a whole, so we are going to analyze the 4 main indices that represent the most important sectors of Wall Street.

But before jumping into the pool, another clarification. A generalist index such as the SP500 or the Russell 2000, since both are based on market capitalization and not on the nature of the company, can be biased depending on the weight of certain types of companies from one time to another.

In other words, today’s SP500 with Google, Facebook and company are not the same as in 1957 when the economy was purely industrial or in 1999 in the midst of the .com craze.

Even with what was stated in the previous paragraph, we are going to take a look at each of these animals in times of tax increases.

The S&P 500 and the rise in interest

The S&P 500 is unique in that it has a bit of all sector of the economy. As of today, in February 2022, the American index has the following composition:

To have reference, in 1999, the technology sector had a weight of 29.18% and then fell to 15.85% in 2007. Meanwhile, communication services went from 7.94% in 1999 to 10.8% today.

Now, according to data from the Dow Jones Market, in the last 5 cycles of interest increases the SP500 has done extremely well compared to the periods in which interest rates have fallen. On average, the index has a return of 62.9% with interest increases and 21.1% with interest decreases.

So do we put all our money into the S&P 500? Not so fast. The numbers above are skewed. On average, the periods of interest increases last about 2 years, but in the data that Dow Jones gave us, the almost 10 years of the 2008-2019 period were included, which is somewhat irregular since the gains of the SPX in this period were 243%, which distorts the figures.

If we take that period out of the equation, we find that the average yield of the SP500 in periods of interest increases is 17%, 4 points lower than when interest rates are lowered. Incidentally, according to Dow Jones data, periods of interest declines tend to be longer; which more or less equalizes the thing.

Keep in mind that interest rates go down when the economy is doing poorly and go up when, on the contrary, the wind blows in your favor.

What happens to the Dow Jones when interest rates rise?

Like the SP 500, the Dow Jones has both times performed well. On the one hand, when the Fed presses the button to raise interest rates, on average, the performance of the industrial index grows by 15.2%, while when it lowers it, it revalues by 23%.

Looking at these data, we can say that the Dow feels better about rising interest rates than the SP500. On average, the return of the DJI is 5.4% while the SPX grows almost double annually, marking 10.5%. However, as we can see, in times of high interest, both indices have practically the same return.

Perhaps this is due to the composition of both indices.

How does the Nasdaq Composite react to rising interest rates?

The Nasdaq Composite is, perhaps, the most affected of the 3 because, as I explained at the beginning of the article, the rise in interest affects growth stocks, which are usually technological, which in turn are the main components of this index.

In times of high interest, the Nasdaq has a return of 17.9%, very similar to that of the SP 500 but pay attention to the data. If we compare the performance of the Nasdaq with a climate of low interest, this is 32%, that is, its growth has been reduced by almost half.

For this reason, the fall of January 2022 should not surprise us at all.

And what happens to small caps when interest rates rise?

To understand the behavior of small caps a little better, let’s take a look at the Russell 2000. This index, made up of small and mid-cap stocks, returned 16.62% during the 12 months after the interest rate hike.

Taking into account that the average annual return of the index is 10%, we can say that it is not doing badly at all, once the uncertainty of the rise in interest passes.

We are concluding

As we have seen, the rises in interest slow down the growth of the main indices in the United States a little. In part, because growth companies are affected and also because capital is not cheap enough for investors to borrow to put it all into the stock market.

However, what history tells us is that the sky does not fall when interest rates rise. In fact, negative returns were only recorded in all 3 indices after the rise in the period between 1999 and 2001.

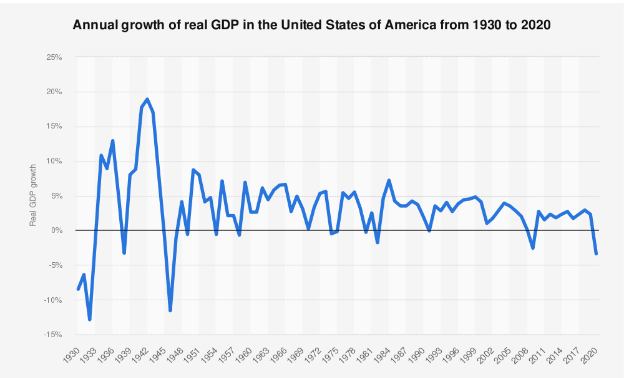

It is true that the prospects for the current rise in 2022 have an extraordinary component, which is the fact that the economy seems to cool down this year. But there is also a lot of alarmism in that sense, the United States will grow 3.2%, well above the average 2% which it usually does.

In short, compadres Zumiteros, the best investment is in the long term so that these potholes are just little spots on our path to glory.